China Marketing Insights Monthly Newsletter [June 2022]

Hello,

Welcome to our June Newsletter.

In this issue, we start with a 6.18 Mid-Year sales strategy. While the top 3 KOL will be greatly missed this year (the latest being “lipstick king” missing from live-streaming since Jun 3rd), there are several other highly effective strategies to implement across Xiaohongshu (or RED), Douyin, Bilibili, Weibo, Zhihu & more. Read our summary & request more details on how to be effective for every sales season.

Private traffic is very relevant and important to have as an effective 6.18 strategy. In this consumer brand report, we detail the nuances of public & private domain traffic, the most effective strategies, touchpoints, and examples. We examine three key industries – beauty, food & beverage, and home appliances.

We have 2 key reports – the 2022 China Male Consumption report and insights from 2022 China Video consumption trends.

Chinese have a habit of giving gifts to make friendly contacts, especially when visiting relatives and friends who have been away for a long time. But as the demographic changes – Gen XYZ, the most influential generation in consumption, has different trends in consumption and gift-giving. Read about the top 8 trends for gifting among Gen XYZ.

In the App of the month, we look at Snail Sleep – an intelligent sleep monitoring app that provides users with intuitive sleep advice services. We look at its functions, advertising opportunities & examples from brands.

Sincerely,

Mia C. Chen

CEO & Co-Founder of OctoPlus Media

618 MID-YEAR PLATFORM PROMOTION LAUNCH STRATEGY

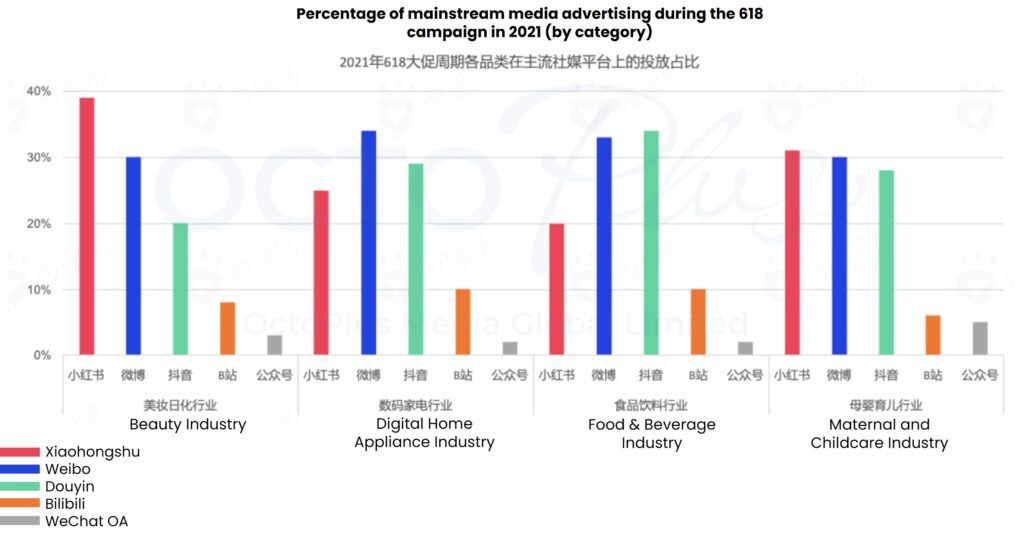

618 is the second-largest and most important shopping festival in China, while Double 11 is the largest shopping festival. From June 1st to June 18th every year, China’s e-commerce landscape is full of large-scale promotions and discounts on the hottest products of the moment, so it is an important large node of the year for major brands. This year, Douyin kicked off as early as April 26, and Kuaishou also started to build momentum for 618 on 520. Even JD.com, Pinduoduo, and Taobao officially launched the 618 promotion on May 23 and 26 respectively. According to “618 E-commerce Social Media Play Panorama Early Insights (2022)” (published by Weiboyi), the following summarizes the relevant strategic content of brands on social media platforms during the 618 periods for reference.

Category and content delivery

First of all, beauty cosmetics and daily chemicals occupy the first place in the category, followed by IT Internet. Others include the maternal and child care categories that tend to use the Xiaohongshu + Weibo + Douyin launch strategy like beauty cosmetics; There are also food and beverage and digital home appliance categories that tend to be placed on Weibo + Douyin + Bilibili for launch strategy. Contents delivery of related categories:-

Beauty cosmetics, daily chemicals products, maternal and child care: focus on vertical content, mainly based on users’ specific needs and hobbies, etc.

Digital appliances: Demonstrate multiple-use effects of products to reach consumers

Food and beverage: Use daily life content to create the hottest and most popular products through Douyin and Xiaohongshu

Social media platform marketing and gameplay

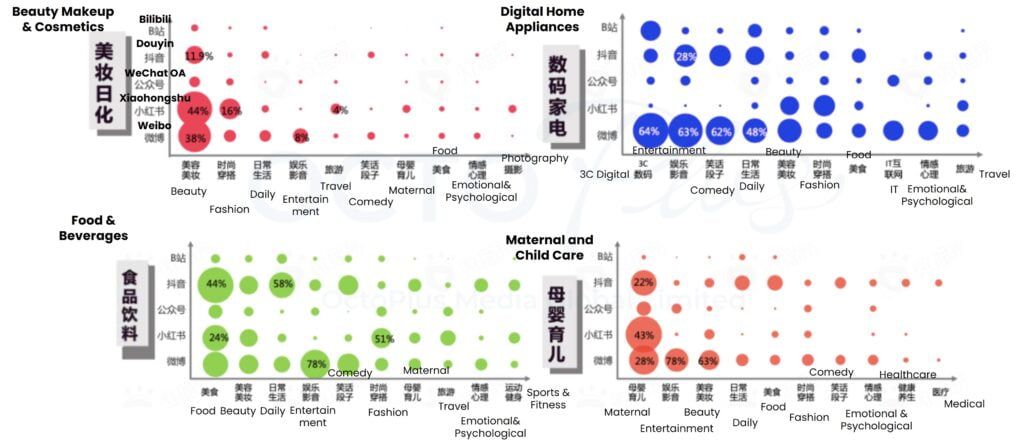

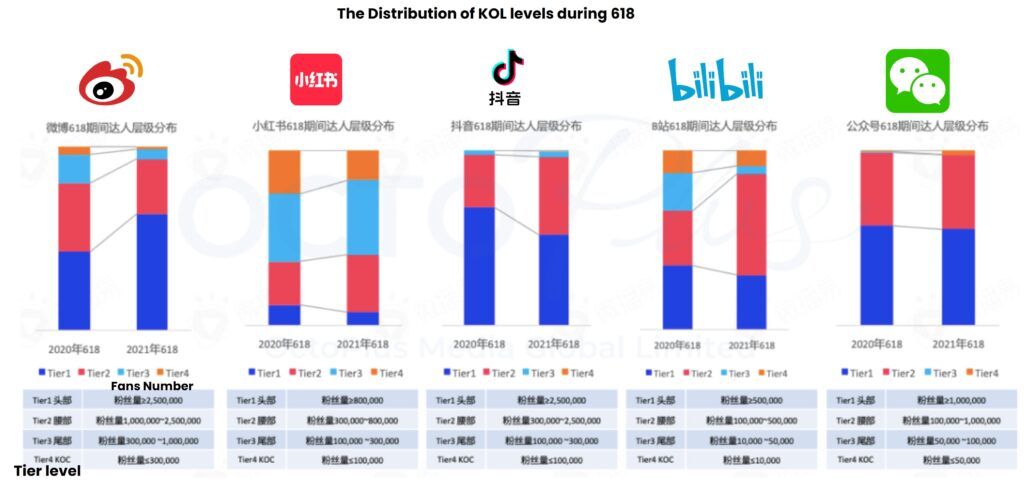

The trend of each platform is different, thus choosing a suitable platform for a category will have different results, while the selection of influencers will also be different. For example, Xiaohongshu skews toward mid-tier and low-tier influencers, Weibo has a trend of choosing top-tier influencers, while Douyin and Bilibili are mid-tier influencers.

1. Xiaohongshu

Platform role: First station for product longing, uses the scene content to publish notes to create word of mouth, let mid-tier influencers and KOC share real content, release product selling points and endorse the brand, which is conducive to the brand’s completion of longing and purchase

Marketing / Strategy: Complete the layout of cooperation notes in the node ahead of time, use the search popularity to seize the traffic opportunity, and continue to publish notes to maintain the traffic and popularity, especially the peak reading time of different categories of notes is different. For example, the beauty category highly follows the trend of e-commerce nodes, while home decoration traffic peaks during 618 big promotions.

2. Douyin

Platform role: Grow products longing consumers precisely through watching the content videos of popular products, increase the brand voice, and increase traffic through live broadcasts during the node period and convert into sales. The most common way of live broadcast e-commerce is through influencers, product promotion capacity is higher compared with the ability of self-broadcasting of merchants, and sales volume is also very impressive.

Marketing / Strategy: The top three core categories in 2021 include pre-sale and the official period are formal apparel, lingerie, food and beverages, and household items. Apparel and lingerie categories are promoted via top, mid, and low-tier influencers and KOC, the warm-up period and the precipitation period focus on the mid and low-tier influencers and KOC, and the bursting period focuses on the release of the market voice through top-tier influencers. The beauty category tends to choose a large number of KOC amateurs for word-of-mouth brand building; the daily necessities category adopts a combination strategy of low-tier influencers and KOCs.

3. Bilibili

Platform role: Use the uploader of high-quality delivery content to reach target consumer groups at multiple points, and influence user decision-making by extending the period of high-quality products promotion content, displaying product links in multiple forms and providing deep-link to complete users of product planting and purchase cycle.

Marketing / Strategy: Users have high spending power, thus the target categories are suitable for high-unit price commodities such as 3C digital and automotive categories. The mid and low-tier uploader is mainly the launch trend of e-commerce nodes at B site because the activity at B site is relatively high and the penetration of circle is strong, and the cost of brand launch is low too.

4. Weibo

Platform role: The first station of the product announcement and distribution through marketing and entertainment top influencers will arouse Weibo’s attention to hot searches, attract the attention of users in the brand/product core circle, and later drive the sales conversion of big promotion nodes.

Marketing / Strategy: Use celebrities + endorsements + topics + influencers to collaborate in multiple ways, such as KOL and KOC publishing and sharing joint gift boxes; celebrity/top influencer emotional story content or creative TVC publicity and promotion core selling points to catch consumers’ attention, heating traffic to increase the brand discussion.

5. Zhihu

Platform Role: The discussion space is opened with professional Q&A, and good things are recommended to create a heated discussion top list to promote conversion. Zhihu has set up 618 product longing groups, covering different topic owners by providing professional content support for different categories of brands.

Marketing / Strategy: “618 Zhihu Good Things List” provides the brand with the opportunity to enhance the exposure of “hot selling products”, by displaying the good products in the content topic discussion, thus the discussion of brands products has sustainable exposure, and afterwards through “Zhihu Good Things Promotion Contest”, it will set off an upsurge of interaction, use multiple traffic resources to reach a wide range of influencer who promote products and drive the atmosphere of Zhihu for the promotion of the product.

Marketing strategy recommendation

Preparation period: From May 10th to the end of May, as the pre-sale period, brands can conduct a wide range of pre-heating and product previews during this period, it is recommended that brands choose multiple platforms to increase the amount of product longing, take the lead in harvesting the first wave of users’ favour.

Sprint period: From the beginning of June to June 13, during the period of making a voice, the brand can choose a combination of product selling points or a special selection of pan entertainment platforms for combination, focusing on the continuous fermentation of voice.

Explosion period: From June 14th pre-sale period to June 20th, brands can integrate the early penetration effect for rapid transformation, and focus on the platform’s in-station operation, at the same time, it efficiently diverts traffic through social media platforms and joint e-commerce platforms.

For more details, please contact us.

INSIGHTS REPORT - 2022 CHINA MALE CONSUMPTION

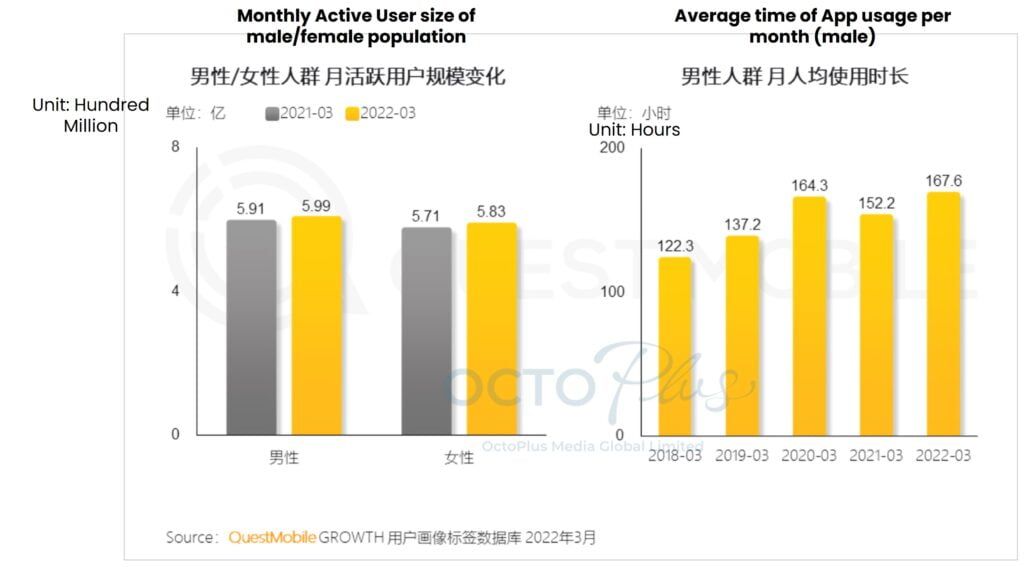

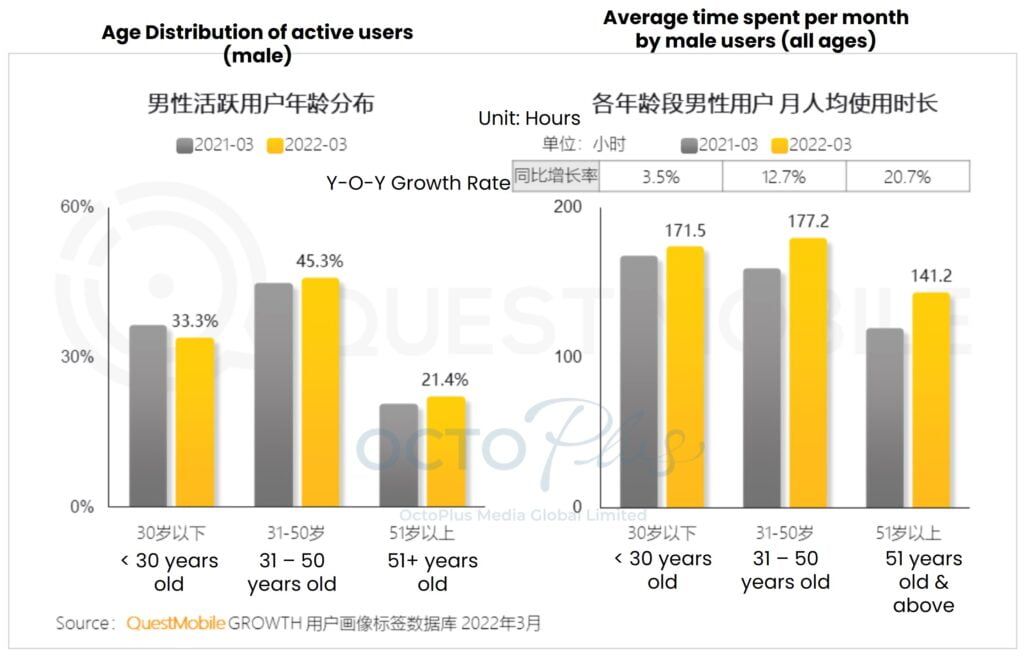

According to QuestMobile data, the average monthly usage time of APPs by China men has increased to a new high in the same period, reaching 167.7 hours, and the monthly active users are close to 600 million.

The 31-50-year-old middle-aged group is the main group driving the growth, and its active proportion and usage time surpass that of young users, up to 177.2 hours, compared with 171.5 hours in the stage under 30 years old. The proportion of first- and second-tier cities are mainly users under the age of 30, and as the age group increases, the distribution of users gradually tilts into the lower-tiers markets.

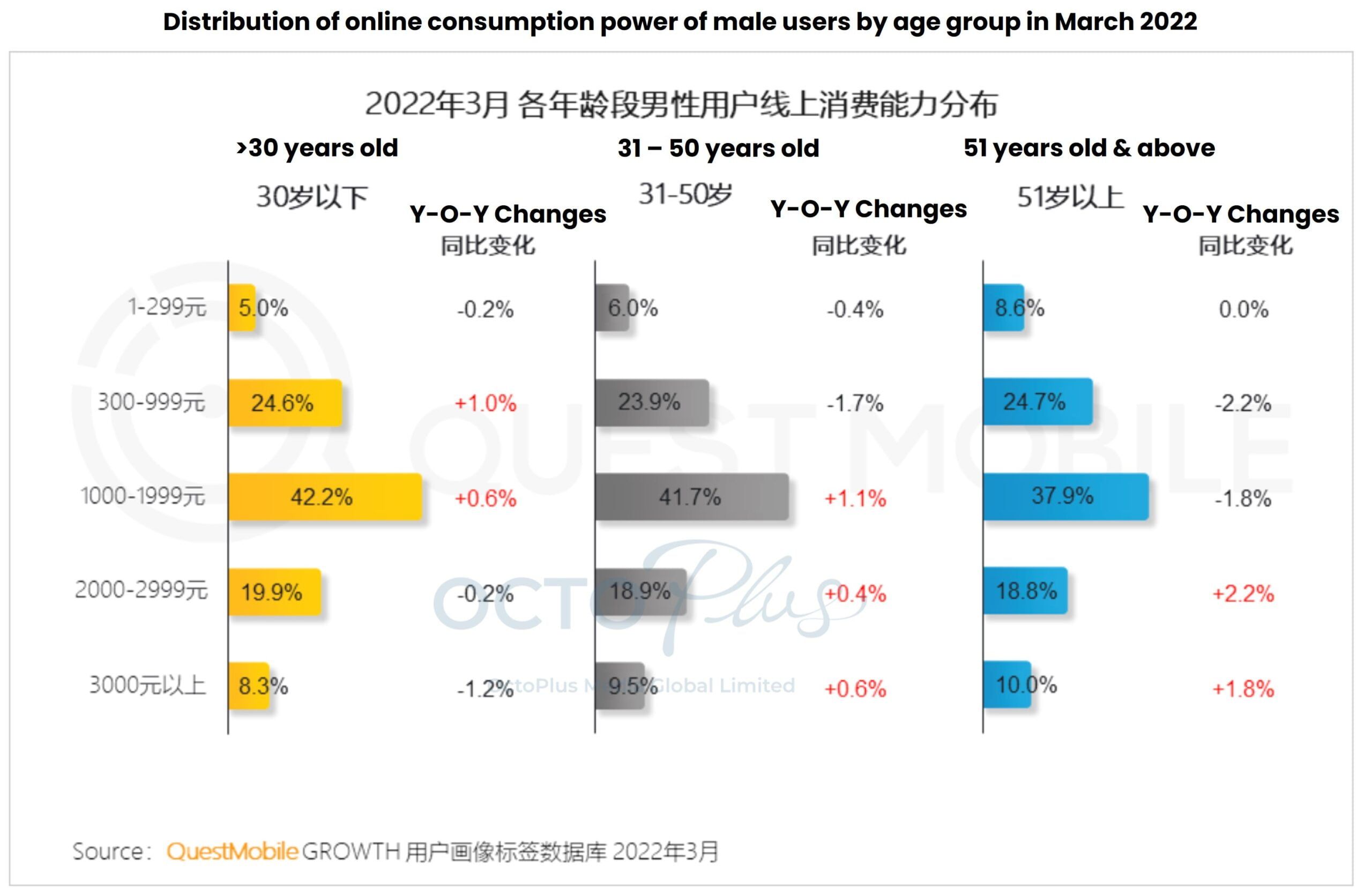

According to data observation, the proportion of online spending power of 31-50-year-olds continues to grow. In contrast, 51-year-olds have outstanding performance in large-scale consumption (consumption range of more than 2,000 yuan). It can be seen that the online consumption potential of China’s middle-aged and elderly users is gradually expanding. The online consumption of young males ranges between 300-1999 yuan.

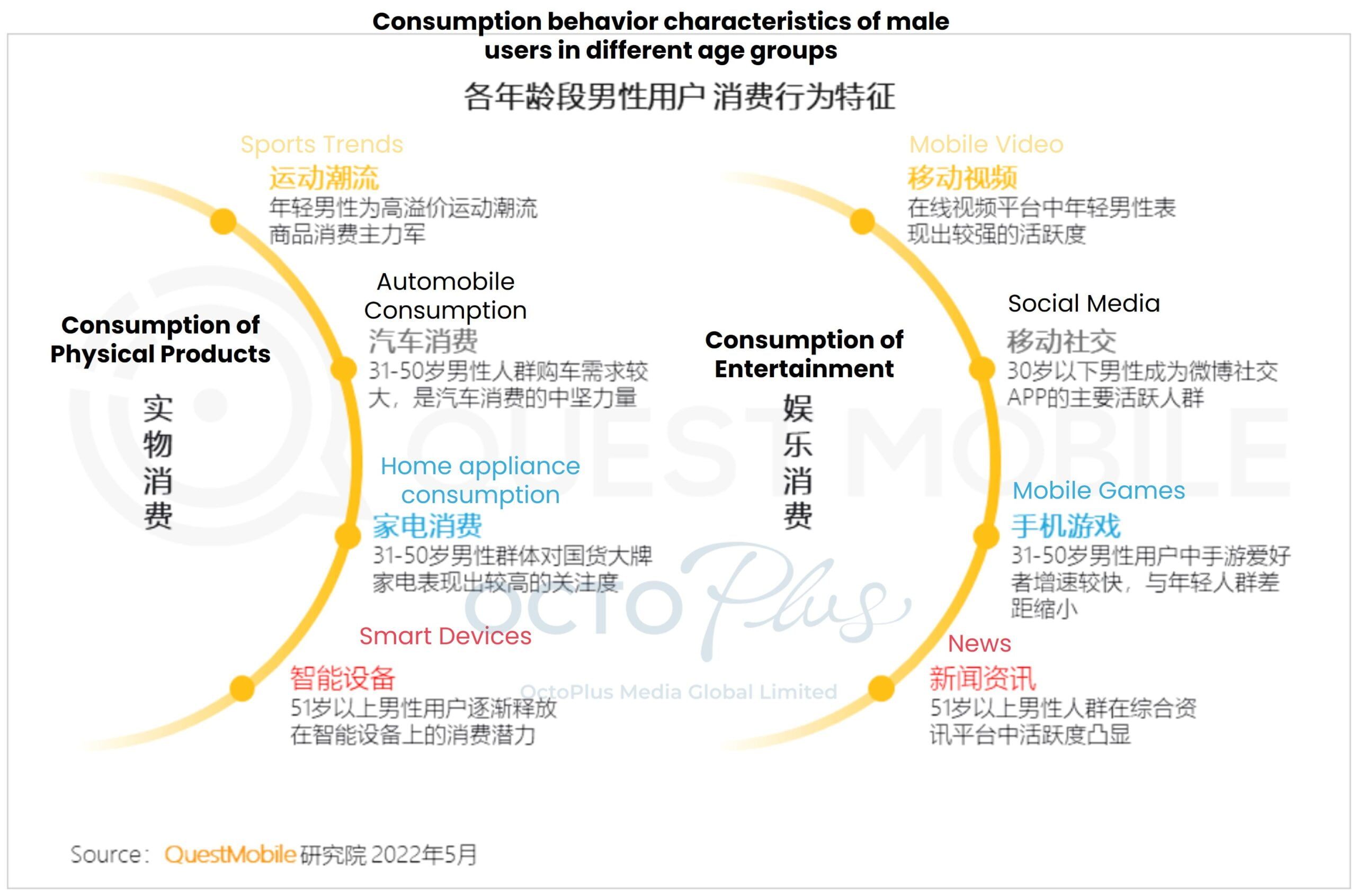

There is a sharp contrast in the characteristics of China male user group portraits. Young male users’ willingness to consume is inclined to entertainment figures, and they are also the core group of sports trend products. 31-50-year-old male users have an online spending power of more than 1,000 yuan with the proportion of users being 70.1%. They are also the main force of consumption in China and are also the core group of automobile home appliances (large-scale physical goods). As men over the age of 51, they tend to be active in news and information platforms, and gradually release their potential in the consumption of smart devices, and their views on consumption have also begun to change.

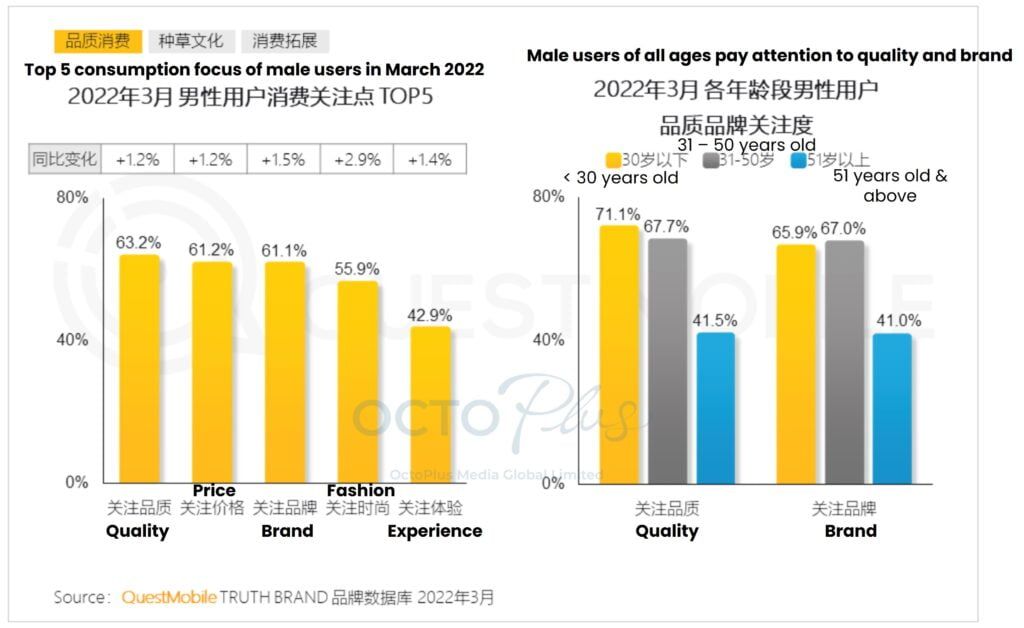

Based on the overall improvement of China’s male consumption awareness, the increasing demand for quality consumption and the gradual diversification of the male consumer market, new trends have quietly emerged. In addition to price, quality and brand have become the decision-making points that all age groups pay attention to, and the main customer group of beauty brands has expanded to young male users. The 31-50-year-old users are more active in various product longing platforms, and their attention to longing and live broadcast platforms has increased. In addition, 51-year-olds have also begun to pay attention to beauty products and show interest, expanding into the trendy consumer circle. 31-50-year-old male users not only pay attention to quality but also consider the factors of their consumption based on brand recognition, focusing on brand attention is the highest among other age groups, as high as 67%.

It can be seen that this gradually evolving new trend has begun to change the tendency of China male users to consume online, gradually expand the ability of male online consumption, and even open up diversified markets, such as beauty and luxury goods. The new “secret code of traffic” of major product longing platforms is more about male-related topics. It can be seen that China male consumption is increasingly influenced by KOLs, and at the same time, it brings diversification and unlimited marketing possibilities to major brands.

To learn more, please contact us!

12 INSIGHTS FROM 2022 CHINA’S VIDEO CONSUMPTION TRENDS

Under the background of the impact of the pandemic, the categories of live broadcast products are becoming more and more abundant, and they continue to meet the diversified consumption needs of the China masses, promote the prosperity and development of the video account e-commerce ecosystem, and open the video account live broadcast models. With increasingly mature live broadcast e-commerce platforms and more diversified consumers, with the normalization of the epidemic, the sales amount of live broadcast products in China has increased by 15 times in the past year.

The positive cycle of the video account content ecology has attracted more and more outstanding creators to complete the accumulation of UGC original content, while improving user retention and interaction, bringing more commercialization opportunities for creators. As a rising star, the WeChat video account, coupled with WeChat’s huge user base, combined with various scenarios of the WeChat ecosystem, and the online and offline linked account matrix layout, have created a strong combination. Nowadays, video accounts with rich and diverse content improve the product experience and combine and increase support for creators and merchants. With the per capita usage time of video accounts rising, more and more business brands are entering the video account, and users’ consumption habits are gradually formed, the popularity of live broadcast e-commerce continues to rise.

The “2022 Video Account Consumption Insight Report” released by Youwant Data analysed 12 insights on the changes in video account consumption trends across various dimensions.

Insight 1: A preference for food, beauty, and fashion

Despite being affected by repeated epidemics this year, consumers’ preference for a decent life is still unimpeded. Even if travel is restricted, consumers still love to eat, and they love beauty as well as fashion. According to the report, the top 5 categories of consumer preference include men’s and women’s clothing, food and beverages, skincare, daily necessities, and shoes and bags. Men’s clothing and women’s clothing (29.44%), food and beverages (28.64%), and skin care (14.05%) occupy the top three consumer favourite categories, while daily necessities are only 7.66%.

Insight 2: The newly emerging consumer power – the “silver-haired group”

With the increasingly mature and perfect live broadcast e-commerce platform, a new consumer force that cannot be underestimated is emerging. This group of “silver-haired group” who are active in video accounts, in addition to sharing the various aspects of life, the passion and spending for fashion and wear are not inferior to young people, and silently supports the blue ocean market.

Insight 3: The “her economy” consumer market that occupies “half of the market”

Occupying “half of the market” of the female consumer market, with the change of consumption consciousness, “pleasure consumption” has gradually become the trend of female consumption. The ladies of the video account began to pursue intellectual elegance and fashionable “pleasant” consumption characteristics to show women’s intellectual beauty, independence and self-confidence.

Insight 4: High customer unit price consumption market has great potential

With a wide range of video account consumer groups and a certain consumption power, operators can even increase conversions by generating deep connections with users through private domains. For products with high customer unit prices such as gold jewelry or digital home appliances, the trust relationship established in the private domain has gradually released the consumption potential. According to the data of Hongrenzhuang service account, after the double 11 and China Gold cooperation GMV broke 10 million last year, the “3.8 Goddess Festival” – International Women’s Day shopping festival has been on the rising.

Insight 5: Consumers restrain rational consumption

Based on the restraint of rational consumption by China video account consumers, practical and good things with a price lower than 100 yuan and high quality-price ratio performance are more likely to arouse the purchase desire of video account consumers, and the sales volume is expected to exceed 71%.

Insight 6: Seasonal consumption in spring and summer

During the change of seasons, consumers want both stylish and fashionable clothes and also new clothes that are versatile and slim. The changing seasons of spring and summer is the moment of consumption. It seems that a trend has formed, and the best-selling clothing is temperament shirts, short-sleeved T-shirts, fashionable sweaters and classic small suits.

Insight 7: Daily essentials, also love the life of casual snacks

In addition to the daily necessities, China video account consumers also love to buy fresh snacks and live an exquisite life. The hot-selling food and drinks on the video account not only include grain and oil seasoning, meat, poultry and eggs, dairy baking, and cooked food buns, but also seasonal fresh and casual snacks.

Insight 8: Refined skincare

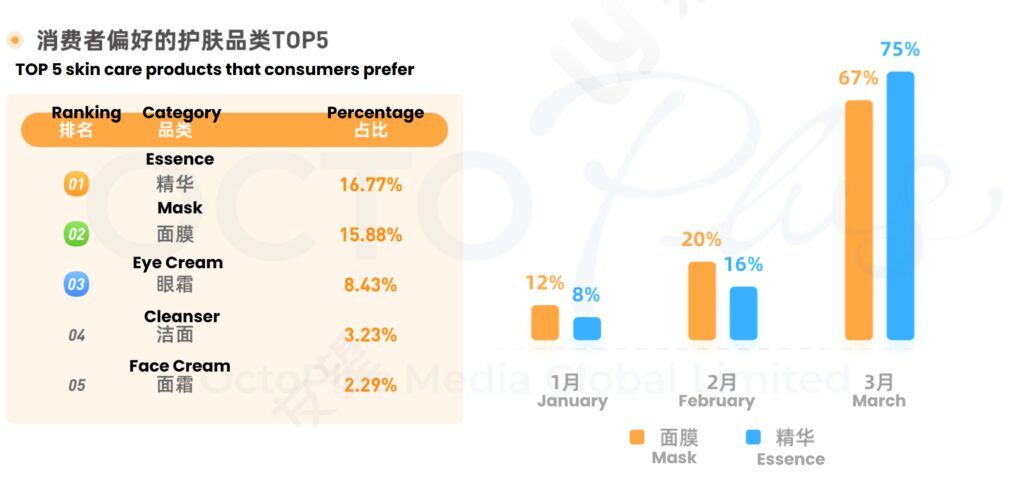

Consumers of Chinese video accounts are not only increasing in demand for delicate skin care among women, but male consumers are also paying more and more attention to this aspect. Consumers’ preferred skin care products show that consumers’ demand for essences and facial masks is much higher than for facial cleansing products. It can be seen that simple facial cleansing no longer meets the needs of video account consumers. According to statistics, the sales of facial masks and essences have a clear growth trend from January to March. It can be seen that the market for essence and mask products has huge development potential.

Insight 9: Exquisite dress up

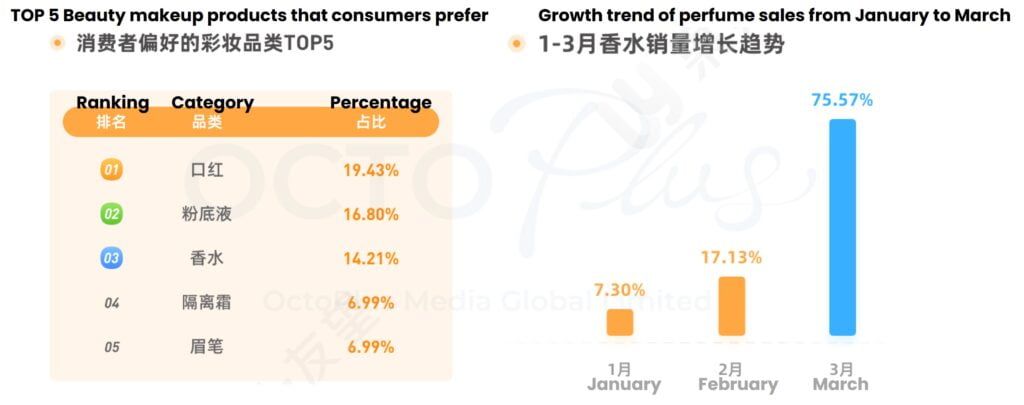

With the increasing demand of Chinese consumers for the quality of life and the widespread popularity of the concept of self-pleasure, more and more consumers are buying makeup products for exquisite dress up, and the room of development of the perfume market is showing a rapid trend. According to the top 5 makeup categories preferred by consumers, lipstick, liquid foundation and perfume are the categories that consumers prefer to buy, and the sales of perfume have increased significantly from January to March.

Insight 10: Specialty food network leads the way

In the online world, consumers who live far from homes can enjoy special delicacies from all over the world. Through the live broadcast of video accounts, consumers can buy special products from 16 provinces (cities) around the world, and good things will be delivered to their homes. The more “earthy” specialities are more popular, the three agriculture bloggers live-stream their own agricultural products on site, and the special agricultural specialities sold by their video accounts are selling well.

Insight 11: “Out of the Circle” Live Broadcast

If you want to increase the purchase rate and prolong the time users watch live broadcasts, you can set up various drainage models when the live broadcast promotes goods, which can directly absorb the flow of the live broadcast room and make the products hot-selling.

Insight 12: Convenient purchasing channels

After the shopping cart function of the video account is launched, the one-click purchase brought by it is convenient for consumers to purchase and it improves the income of creators. When the video play rate is higher, the exposure to related products is more, and the sales volume is also increased, achieving a positive ratio. According to the data, the hot-selling products related to the video are spicy dried radish, thick leg trainer and tensioner.

According to the statistics of Youwant, 60.13% of the live-broadcast goods on video accounts come from small stores. The convenient purchase channels allow many merchants with supplies to enter the live broadcast platform for free to open stores and sell live broadcasts. As for creators without supply, they can choose to distribute goods in small stores to earn commissions.

However, since March 25th, due to the stricter and more standardized requirements for live broadcast to ensure consumer safety, and the video account has stopped providing window services to individual main stores, the individual can only obtain and purchase goods with a third party that cooperates with video account for the live broadcast.

With the normalization of the epidemic and the prosperous development of the video account e-commerce ecosystem, the user participation in live-broadcast video accounts will continue to grow, and the categories of live broadcast products will gradually be enriched, which can continue to meet the consumer needs of the vast number of China users, thus the development potential of live-broadcast video accounts is even greater.

Contact us to download the full report!

2022 CHINA PRIVATE TRAFFIC STRATEGY FOR CONSUMER BRANDS

The most popular operation model for China brands is the combination model, which uses the combination of a public traffic platform touchpoint and brand private traffic channels to pull the brand’s traffic to the highest point.

So what is a public traffic platform touchpoint? What is a private traffic channel?

The operation mode between the two will obtain their own traffic, among which the public traffic is the traffic that every customer can purchase or obtain through public channels in the public traffic. Some public traffic platforms, such as Weibo, Taobao, Douyin, Toutiao, Tencent, etc., are all platforms that can purchase traffic through public channels.

Private traffic is the traffic that customers can freely use repeatedly without paying, and which can be accessed at any time. Compared with the major public traffic platforms, it belongs to the customer’s “private asset”. For example personal WeChat account, community, circle of friends, etc.

The biggest difference between the two is that there is fierce competition in public traffic, and there may be dozens or hundreds of peers competing for the same traffic. However, private traffic only belongs to the merchant itself, and there is no peer competition.

QuestMobile recently released the “2022 Consumer Brand Private Traffic Layout Strategy Insight Report“. According to the data, as of March 2022, the number of official accounts of various public traffic platforms has increased significantly compared with the same period last year. Among them, the four major modules of customer acquisition and drainage, user retention, consumption conversion, and precision marketing have basically matured. The following summarizes the relevant strategic content of consumer brands using public traffic platform touchpoints + brand private traffic layout as a reference.

The public traffic platform and the private traffic contact point have become the new private traffic operation ecology

With the subsidence of the mobile internet traffic bonus, the overall advertising cost has further increased, and the brand has realized that it is deeply cultivating the existing users, and the private traffic operation has been launched accordingly. Through platform closed-loop construction, brand self-broadcast traffic support, and open technology ecology to attract brands to settle in, and achieve a win-win situation between the platform and the brand.

The overall operation mode of the private traffic mainly includes 4 modules, namely customer acquisition and drainage, user retention, consumption conversion, and precision marketing. The following are different industries, which are laid out through different private traffic methods.

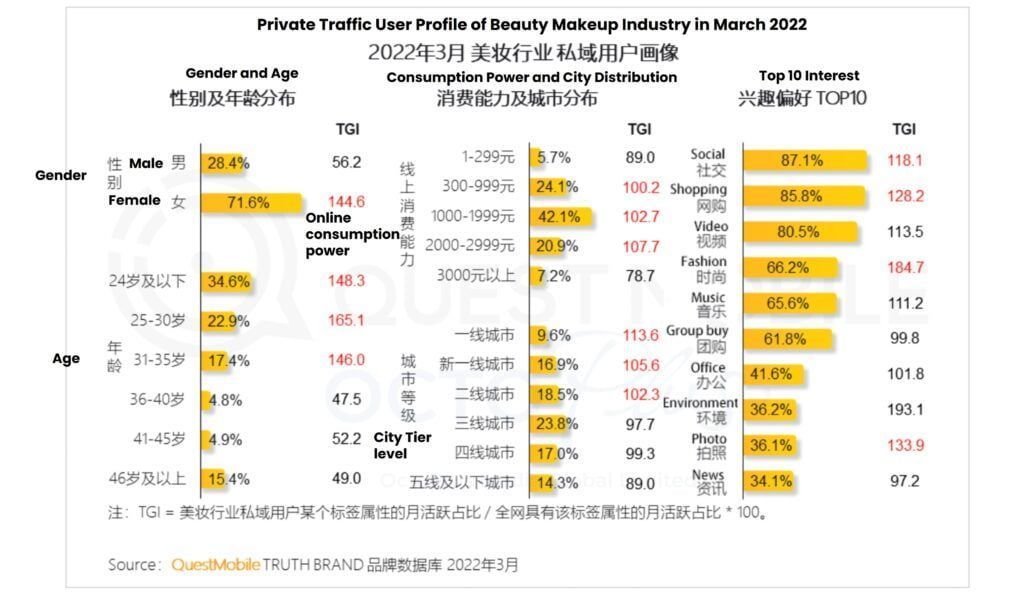

1. Beauty industry

According to the report, the users of beauty private traffic are mainly concentrated in:

- Women under the age of 35

- A significant proportion of first- and second-tier cities

- Users show obvious “beauty-loving” characteristics such as taking pictures and fashion

- Social and online shopping preferences are conducive to social operation and secondary conversion in the brand’s private traffic

Therefore, most of the beauty industry is dominated by official accounts and mini-programs. Beauty brands can be divided into two types, namely traditional beauty (Watsons, L’Oreal, etc.) and cutting-edge beauty (Huaxizi, Perfect Diary, etc.). Due to the characteristics of offline stores, traditional beauty brands use mini-programs as an important position to gather traffic; while new and cutting-edge beauty brands will focus on online sales on their official accounts.

Simply put, traditional beauty brands gather online and offline traffic through the “store + mini-programs” model. On the other hand, cutting-edge beauty brands use official accounts to help brands build momentum, interact with users and achieve conversions through live broadcasts.

The following is the TOP10 list of private domain users of the beauty industry brands, you can refer to:

1. Huaxizi

2. Watsons

3. Perfect Diary

4. Yunifang

5. L’Oreal

6. Dior

7. Estee Lauder

8. Home Facial Pro

9. Colorkey

10. Winona

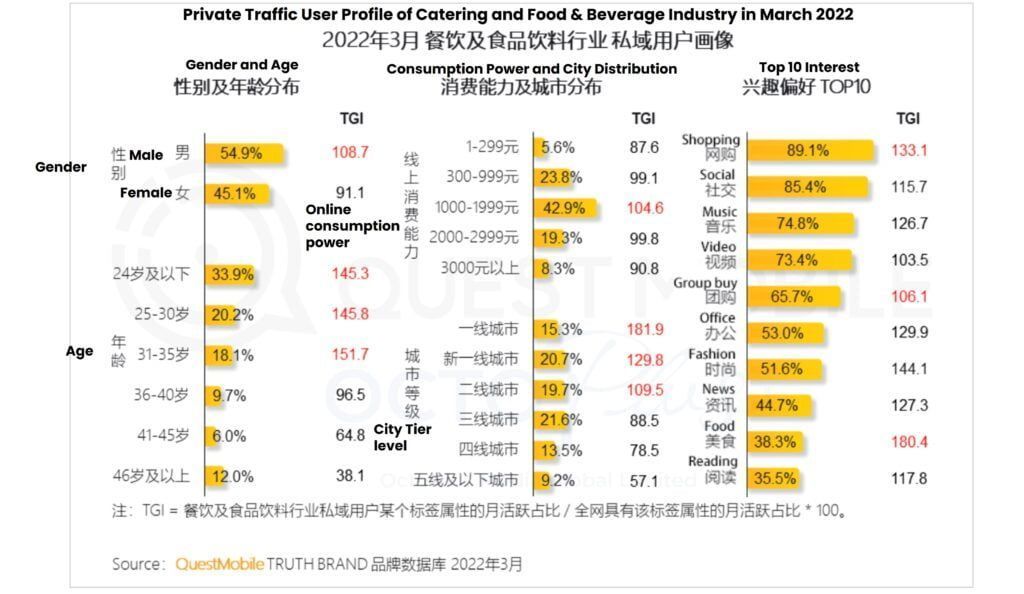

2. Catering and food and beverage industry

From the data point of view, private traffic users in the catering and food and beverage industries are mainly concentrated in:

Young people (24 years old and below)

Interests and preferences are online shopping and group buying

Due to the high offline consumption of chain restaurants, most of them choose “combo ”, that is, the combination of mini-programs + APP. While some brands of dairy drinks or casual snacks will work hard on the operation of the official account + mini-programs. The catering and food and beverage industries focus on the conversion and retention of users in private traffic operations; while mini-programs and APPs undertake the functions of rapid conversion and user precipitation; lastly, the official account achieves brand exposure and centralized transformation.

The following is the TOP10 list of private traffic users of brands in the food and beverage industry, you can refer to:

1. KFC

2. McDonald’s

3. Luckin Coffee

4. Yili

5. Mixue

6. Starbucks

7. Li Ziqi

8. Want Want

9. BESTORE

10. Pizza Hut

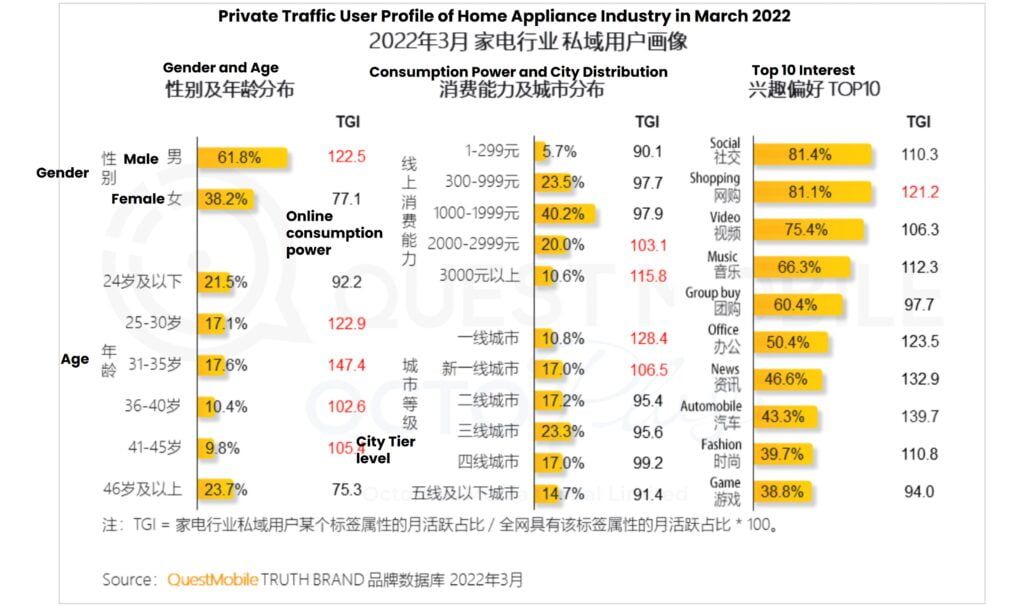

3. Home appliances industry

Data shows that private traffic users in the home appliance industry are mainly concentrated in:

Mostly male

Diverse age structure

First-tier developed cities have high penetration

The behavioural characteristics of users’ online shopping are obvious

As the device access port of smart home appliances, APP has the advantage of natural traffic aggregation, and is used as an important contact point by major smart home appliance brands; while small home appliance brands pay more attention to the operation of the official account + mini-program model.

To put it simply, smart home appliance brands form a closed-loop after-sales within the ecosystem by building rich service scenarios in the APP. While small home appliance brands use the official account + mini-program model to achieve centralized transformation and bring users a convenient operating experience.

The following is the TOP10 list of private domain users of household appliances industry brands, you can refer to:

1. Midea

2. Haier

3. Gree

4. Joyoung

5. Ecovacs

6. Supor

7. TCL

8. Dyson

9. Bears

10. Ya-man

To sum up, different industries have different combination models. However, these combination models can greatly help brands maximize traffic, and then realize a closed loop of conversion and retain users.

For more details, please contact us

2022 CHINA GIFTING CONSUMPTION TREND INSIGHT: FUTURE GIFTING TREND OF GENERATION XYZ

China people have a habit of giving gifts to make friendly contacts, especially when visiting relatives and friends who have been away for a long time, willingness to choose souvenirs as gifts. But as the demographic change, Gen XYZ, the most influential generation in consumption, has different trends in consumption and gift-giving.

Who is Gene XYZ?

“Gen X” refers to those born in the mid-1965s to the late 1980s; “Gen Y” refers to those born from the 1980s to the 1995s; and “Gen Z” refers to those born from the 1995s to the 2010s.

Recently, Leadleo Research Institute conducted a survey on “The Future Gifting Trend of XYZ Generation” to observe their overall consumer industry trends.

2022 Holiday Gifting Overview for Generation XYZ

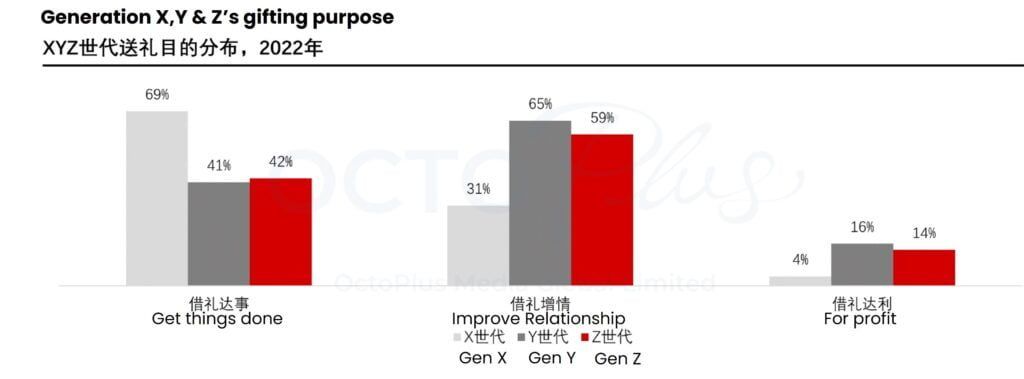

According to the report, in terms of the purpose of gift-giving, 65% of Gen Y and 59% of Gen Z hope to improve their relationship through gifts, while 69% of Gen X hope to achieve their purpose through gifts.

What about the gift-giving trends in Gen XYZ?

Trend 1: Experiential gifts become the first choice for Gen Z gifts

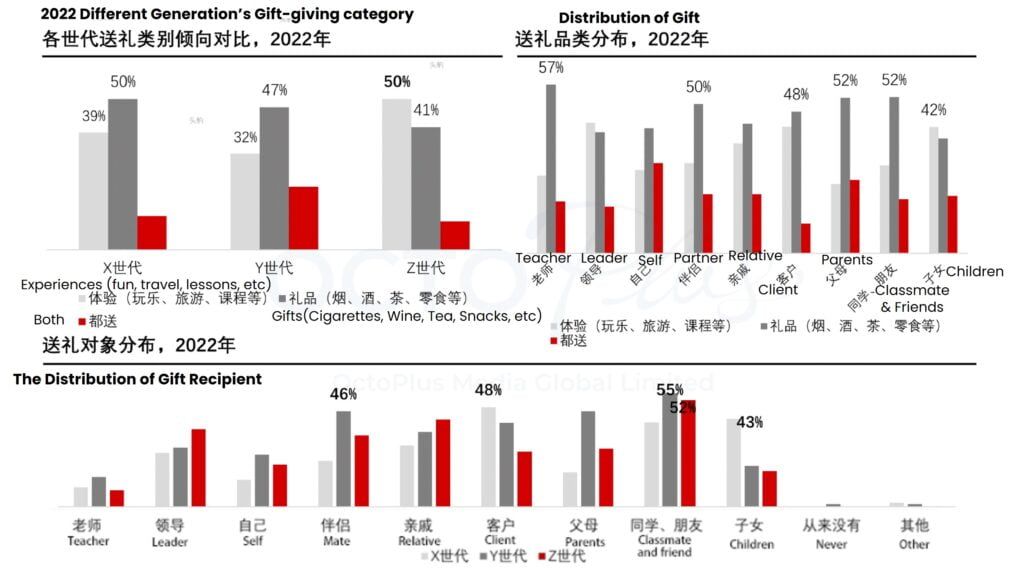

The current phenomenon of high homogeneity in the gift market has led to a decline in the experience of gift recipients and gift-givers. Gen Z believes that the high experience and customized experience brought by experiential gifts will be more attractive than homogeneous gifts, so they will give priority to experiential gifts (such as play, courses, travel, etc.). In contrast, in Gen X and Gen Y, taking into account factors such as the understanding of the recipient’s preferences and social distance, the gifts given to customers are mostly gifts (such as cigarettes, wine, tea, snacks, etc.), and gifts given to children are mostly gifts as an experiential gift.

Trend 2: Home-related gifts have become the mainstream gift-giving

The changes in life and work scenarios affected by the epidemic have led to a gradual increase in the importance of each generation to the home scene, and various electronic products, pets, and lifestyle gifts have become the mainstream of gift-giving. According to the report, gender classification can be seen in gift-giving differences. For example, women pay more attention to the concept of health and beauty in gifts, while men give gifts through high-priced tobacco, alcohol or tea.

Trend 3: Gen X favours in health-care-related gifts, Gene Y and Z favours in healing-gifts

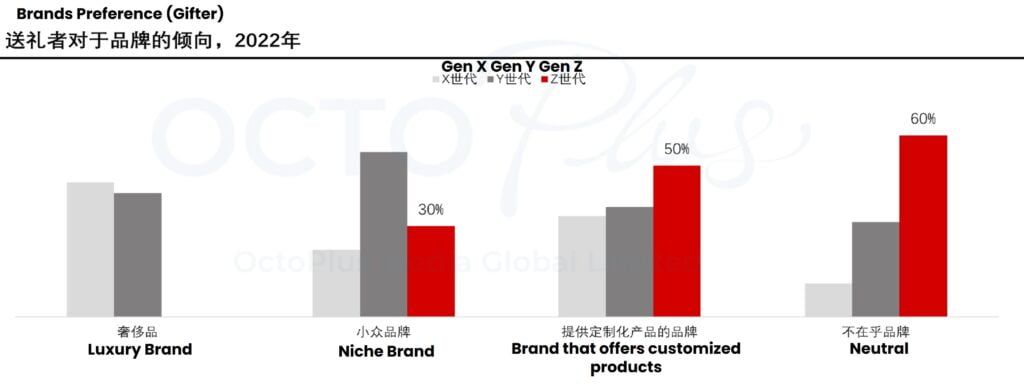

Gen X will pay more attention to health as they grow older, so gift-givers will choose products related to health categories; due to high workload and the trend of younger stress, gift-givers are guided to pay more attention to healing and relaxation when choosing gifts for Gen Y and Z. Given the trend of gift-giving, it can be seen that the same age gift-givers of Gen Y and Z are more likely to determine and understand the preferences of the recipients, and in general gifts and experiential gifts are decided through their own preferences and suggestions from friends. As Gen X focuses on wellness, 31% and 17% of Gen X gift-givers choose electronics and health supplements as gifts, while 15% choose outdoor activities as experiential gifts.

Trend 4: Customized gifts capture a non-conformist attitude

Research and statistics show, gift givers’ ranking of gift consumption and purchase factors are brand, product, service, price and channel, among which brand and product are the decisive factors for gift giving for each generation.

Although brands and products are the decisive factors for gift-givers to purchase products, Gen Z is more receptive to emerging ideas, determining the gifts through social media product longing and personal preferences and paying more attention to customization in gift-giving, and does not care about brands.

Trend 5: With the greatest intention, the price of gifts can exceed the affordable range

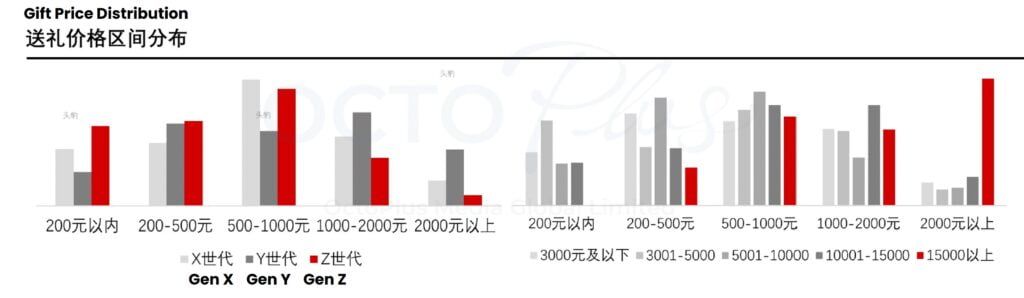

The research shows that although the price is a secondary factor in the consideration of gifts, gift-givers usually refer to the price of the other party’s gift before giving gifts, most gift-givers give gifts in the range of 500 to 1000 yuan, and the price of gifts grows with disposable income. Most Gen X choose the price of gifts based on their level of intimacy with the gift receiver. 80% of Gen X value their greatest intention, thinking that preparing gifts themselves is more able to express their goodwill, thus they are not interested in one-stop services.

Trend 6: Gen Y and Z tend to diversify gift-giving styles

According to the research, 76% of Gen X who prefer preparing gifts themselves are giving gifts for certain purposes, and 78% of Gen Y who prefer one-stop services are for the purpose of giving gifts to increase their affection, gift-giving purpose becomes the main factor in determining the choice of gift-giving styles.

Trend 7: Gift-giving pays more attention to uniqueness and novelty

At present, thanks to the rapid development of big data on various platforms, consumers are more likely to be “longing” via the internet. Therefore, uniqueness and novelty are the decisive factors in deciding whether to buy experiential gifts. Most gift-givers are not sensitive to the price of experiential gifts. As the demand for experiential gifts increases, more unique experiential gifts will be developed.

Trend 8: Social distance determines gift-receiving tendency

The strong functionality of experiential gifts makes the recipients tend to receive experiential gifts, while some recipients prefer to receive gifts in consideration of factors such as social distance and reciprocity. In human society, the recipients of gifts in different scenarios will have different considerations, but in any scenario, the meaning of the gift itself is higher than the value of the gift. 57% of Gen Ys prefer experiential gifts, while 100% of Gen X prefer receiving physical gifts to preserve memory.

Different generations, different ways of giving gifts. Over time, future gift-giving trends may also differ from today.

Contact us to download the full report!

APP OF THE MONTH – SNAIL SLEEP

Snail Sleep was launched by Seblong (Beijing) Co., Ltd. In 2015. It is committed to creating independent research and development of products for sleep and now has become the head brand of domestic sleep monitoring APPs.

Three major business achievements of Snail Sleep:

Independent Research & Development

National Commitment: Recognized as a software enterprise, and obtained national high-tech enterprise certification, FDA filing, ICP telecom value-added license, Class II medical device business license, and EU CC, etc. in 2016. Snail Sleep provides a full range of technical services based on powerful technology and big data

Industrial Highlights: There are currently 75 million+ registered users, the products have won various awards in the industry and have been recommended by the Apple App Store many times. In February 2018, they ranked at the top of the China AppStore Bodybuilding and Fitness List (free) and repeatedly ranked in the TOP1 in overseas regions.

Product Market Overview

APP market: Snail Sleep currently occupies the first place in the domestic market, accounting for more than 30% of the market; the sleep APP with the TOP1 downloads in China

User portraits: post-90s and post-00s account for more than 65%; female users account for 64%; first-tier cities and above account for more than 60%

User attributes: Internet natives, strong spending power; caring for the health and focusing on sleep; high purchasing power, easy to be “longing”

Currently, there are more than 75 million registered users, more than 10 million monthly active users, steady monthly growth of more than 2 million, and a retention rate of 58.38% in the next month.

Snail sleep App Function Introduction

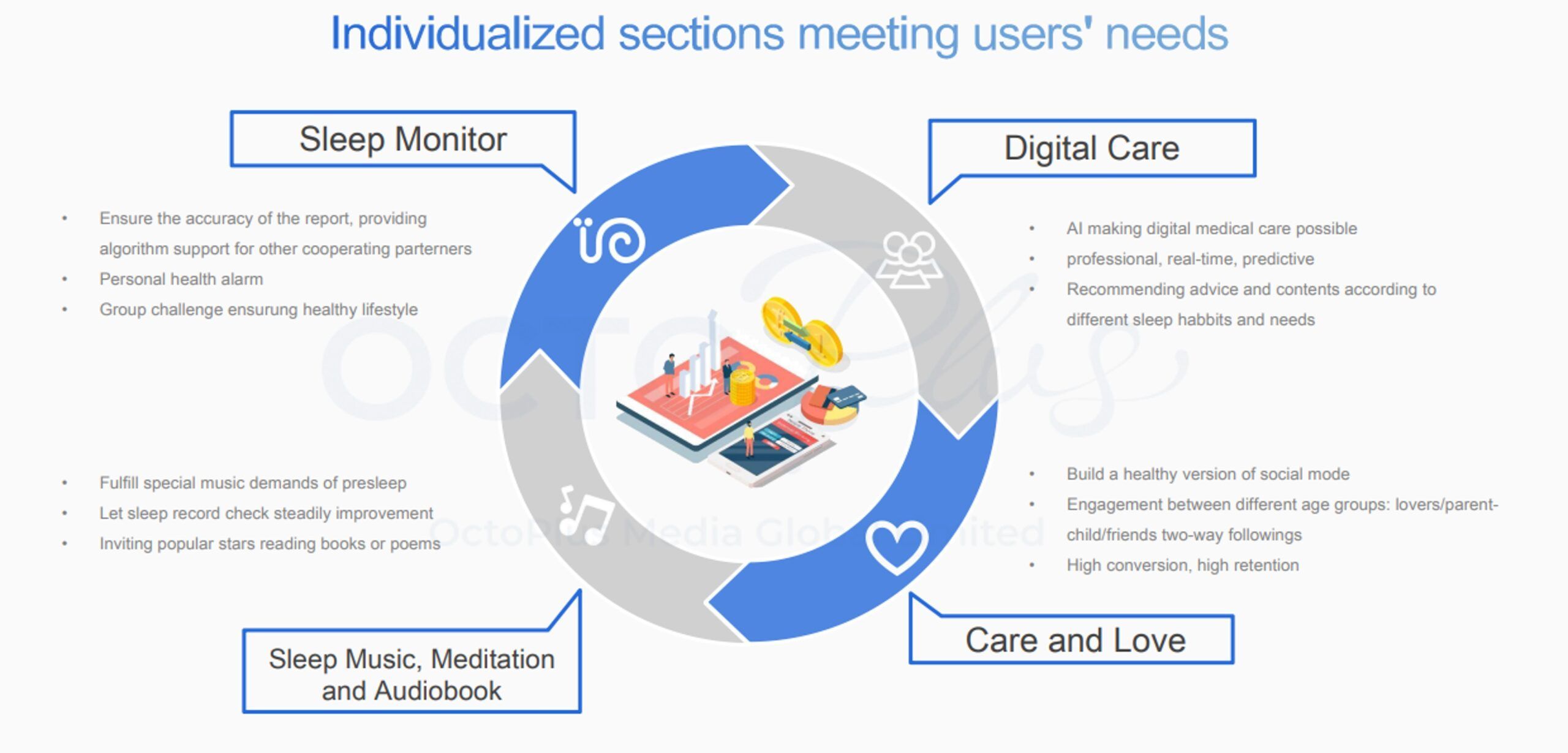

Snail Sleep is an intelligent sleep monitoring app that includes multi-functional partitions and provides users with intuitive sleep advice services.

Sleep Monitor

Sleep Music

Sleep Community

Concern and Love

Why Advertise with Snail Sleep?

1. Snail Sleep provides a brand cooperation method with high customization, high exposure, and high participation. Brands can formulate event gameplay, copywriting, and publicity methods. The 7/21 day event provides a long exposure time, and the brand also attracts users to participate by setting bonuses.

2. Snail Sleep user groups pay attention to sleep health, and the community function is conducive to corresponding needs, helping brand owners to match the corresponding user groups most efficiently.

3. Snail Sleep provides a variety of marketing models to cooperate with communication, which can meet different brand characteristics and meet different brand needs. At the same time, the long event time gives the brand continuous exposure and long-tail communication of the event.

Snail Sleep Advertising Model

Snail Sleep Brand Cooperation Case

Case 1: Snail Sleep Open Splash Ad (Volvo/Buick/Chanel)

Cooperative brands attach importance to the age group, distribution area and an occupational portrait of users in the product, build early brand awareness among young user groups, and guide and educate users to choose their minds.

Case 2: High-quality spots in Snail Sleep, and high clicks lead to potential returns (Xiaomi Youpin)

Select the bedtime monitoring action page banner to launch sleep aid related products, successfully attracting users to click.

Total exposure: 167k+ ;

Total clicks: 157k+ ;

ROI: 1:0.4

Case 3: Launching all operating positions in the station to obtain maximum exposure support, UGC challenge activities to obtain target customers (Swisse)

For more related Snail Sleep advertising cases and advertising solutions, please get in touch with us!

-End of the Newsletter-

Feel free to talk to us

It’s a team with one single shared goal, which is our client’s success. Deliver results for your business now.